Are We in an AI Bubble? What the Numbers Actually Say

Everyone has an opinion on this. The VC optimists say AI is different — real revenue, real infrastructure, real demand. The sceptics point to companies valued at hundreds of millions per employee and ask who, exactly, is going to pay for all of this. The honest answer sits somewhere uncomfortable in between.

If you're the kind of person who has to put a board slide together on this in six weeks, here's the version that doesn't embarrass you at the table.

The Money Is Real. The Returns Are Not (Yet)

Start with the numbers, because they're genuinely hard to argue with.

Global private AI investment reached record levels in 2024 and accelerated further through 2025, with AI firms capturing an unprecedented share of all global venture capital — by some industry estimates, more than half of all VC deployed globally. That represents a dramatic increase in AI's share since 2022. In the first quarter of 2025 alone, AI startups raised tens of billions of dollars, representing a significant concentration of capital in a single sector and a single quarter.

For context: a disproportionate share of early 2025 venture capital went to a small number of AI startups, many of which raised $500 million or more in individual rounds. The infrastructure layer — data centres, compute, hosting — attracted investment at a scale that blurs the line between venture capital and hyperscaler capital expenditure, making precise figures difficult to isolate from public reports alone.

Those are dot-com-era numbers in character. Adjusted for inflation, they may be larger.

The revenue picture is messier. OpenAI generated substantial revenue through 2025 — figures reported by outlets including the Wall Street Journal and the Financial Times have placed it in the range of approximately $10–13 billion, though these are based on reported disclosures from a private company, not audited public filings. According to internal documents reported by multiple outlets in 2024, the company does not expect to turn a profit until around 2030, with significant projected cash burn through 2026 and beyond; those forward projections should be treated as estimates, not established facts. Anthropic grew aggressively through 2025 but remains deeply unprofitable. Meanwhile, early-stage valuations have reached what some investors have described as extraordinary territory — with some companies commanding valuations of hundreds of millions of dollars per employee.

The gap between capital deployed and credible return timelines is the core of the bubble question. Bubbles are defined not by bad technology, but by a vast gap between investment levels and realistic expectations for future profits — a point made by multiple market analysts tracking the current cycle.

The Dot-Com Parallel Is Real, But It's Not Perfect

The dot-com comparison is worth taking seriously, not dismissing.

In the late 1990s, investors poured capital into internet companies based on a genuine technological shift. The internet was real. The companies — most of them — were not. The technology survived. Pets.com did not.

Today, the pattern is similar in its investor psychology. Both eras feature the belief that a technological revolution will transform industries overnight, with capital flowing into startups with unproven business models. The current cycle has produced a large and growing cohort of AI unicorns — CB Insights and similar trackers have documented hundreds globally, with combined valuations in the trillions, though exact counts shift frequently and should be treated as snapshots rather than fixed figures.

But there are differences. The biggest AI companies have real, growing revenue in a way that Webvan and Boo.com never did. Enterprise spending on generative AI grew substantially between 2024 and 2025, with multiple research firms — including Gartner and IDC — documenting significant year-on-year increases, though their specific estimates vary and should be sourced directly for precision. The technology works. The question has never been whether AI is real. The question is whether today's valuations are pricing in realistic timelines for when the returns arrive — and for most companies, they're not.

Erik Gordon, a professor at the University of Michigan's Ross School of Business who has commented publicly on AI market dynamics, has raised concerns about significant overvaluation in parts of the AI market, pointing to early warning signs in infrastructure plays that have already seen violent corrections. CoreWeave, an AI infrastructure company that went public in March 2025, experienced significant post-IPO stock volatility. That's not dot-com 2.0 — but it's not a stable market either.

The distinction that matters for anyone making capital allocation decisions: it's not whether the technology is real. It's whether the valuations reflect realistic timelines. On that measure, significant parts of the market appear priced for outcomes that are 5 to 10 years away.

Enterprise Pilots Are Stalling. Widely.

Here's the thing that doesn't make it into the funding headlines.

A 2026 survey from Writer found that 79% of organisations face challenges adopting AI — a double-digit increase from 2025 — with 54% of C-suite executives admitting that AI adoption is creating organisational fractures. This is despite 59% of companies investing over $1 million annually in AI technology.

Deloitte's 2026 enterprise AI report found mixed results on value. While 66% of organisations report productivity improvements, revenue growth remains largely aspirational — only 20% of organisations are already growing revenue through AI, compared to 74% that hope to do so in the future.

BCG found that 74% of generative AI pilots fail to move to scaled production, stalling in what researchers are now calling "pilot purgatory" due to data quality and governance issues. Only 1% of business leaders reported that their companies have reached genuine AI maturity — where it's fully integrated into workflows across the enterprise.

The bottleneck isn't intelligence. It's plumbing, governance, cost management, and legacy system integration. The honeymoon phase where enterprises would pay for pilots that went nowhere is ending. Financial rigour is arriving. As one industry analyst put it bluntly, 2026 is the year implementation capability becomes more valuable than model access.

For every AI super-user delivering genuinely outsized productivity, there are organisations where 70% of professionals still aren't using AI tools on a regular basis, despite high organisational adoption rates.

This matters for the bubble question. Valuations assume enterprise adoption at scale. Enterprise adoption at scale hasn't happened yet. The gap between where valuations are priced and where enterprise ROI actually sits is one of the cleaner indicators that a correction is more likely than not.

The Infrastructure Bet Is Massive, and It Might Be Overextended

Then there's the energy problem. This one doesn't get enough airtime.

US data centre power consumption is projected to grow significantly through the end of the decade, with multiple forecasts — including from the Department of Energy and independent consultancies — projecting a doubling or more from current levels by 2030. The major hyperscalers — Google, Meta, and Amazon — have each disclosed capital expenditure plans running into the tens of billions of dollars annually for data centre construction, with combined 2025 commitments widely reported as being in the hundreds of billions when aggregated.

The scale of capital being committed raises a legitimate question about payback. Industry analysts at firms including Bain and Accel have noted that realising returns on the current infrastructure buildout requires AI revenue to materialise at a scale that current industry figures don't yet approach. Bain, in particular, has published estimates suggesting that meeting projected compute needs by 2030 would require AI revenue growth of a magnitude that far exceeds current run rates — though their specific figures should be sourced directly from their published reports.

The nuclear play has become a proxy bet for how serious tech companies are about the infrastructure gap. AWS locked in a long-term power purchase agreement for capacity from the Susquehanna nuclear plant in Pennsylvania. Microsoft, Google, and others have made similar moves. Small modular reactors are attracting billions in speculative investment.

But nuclear faces hard physical constraints. Large reactors take between five and eleven years from breaking ground to power delivery. Construction costs for nuclear run significantly higher than natural gas per kilowatt. Several high-profile SMR companies have delivered zero commercial-scale operations despite raising hundreds of millions, with share prices well off their peaks.

The infrastructure bet assumes AI demand will continue to grow exponentially and that new power supply will arrive on schedule. Both assumptions deserve scrutiny. Not because the technology fails, but because the timelines are being priced as though they're guaranteed.

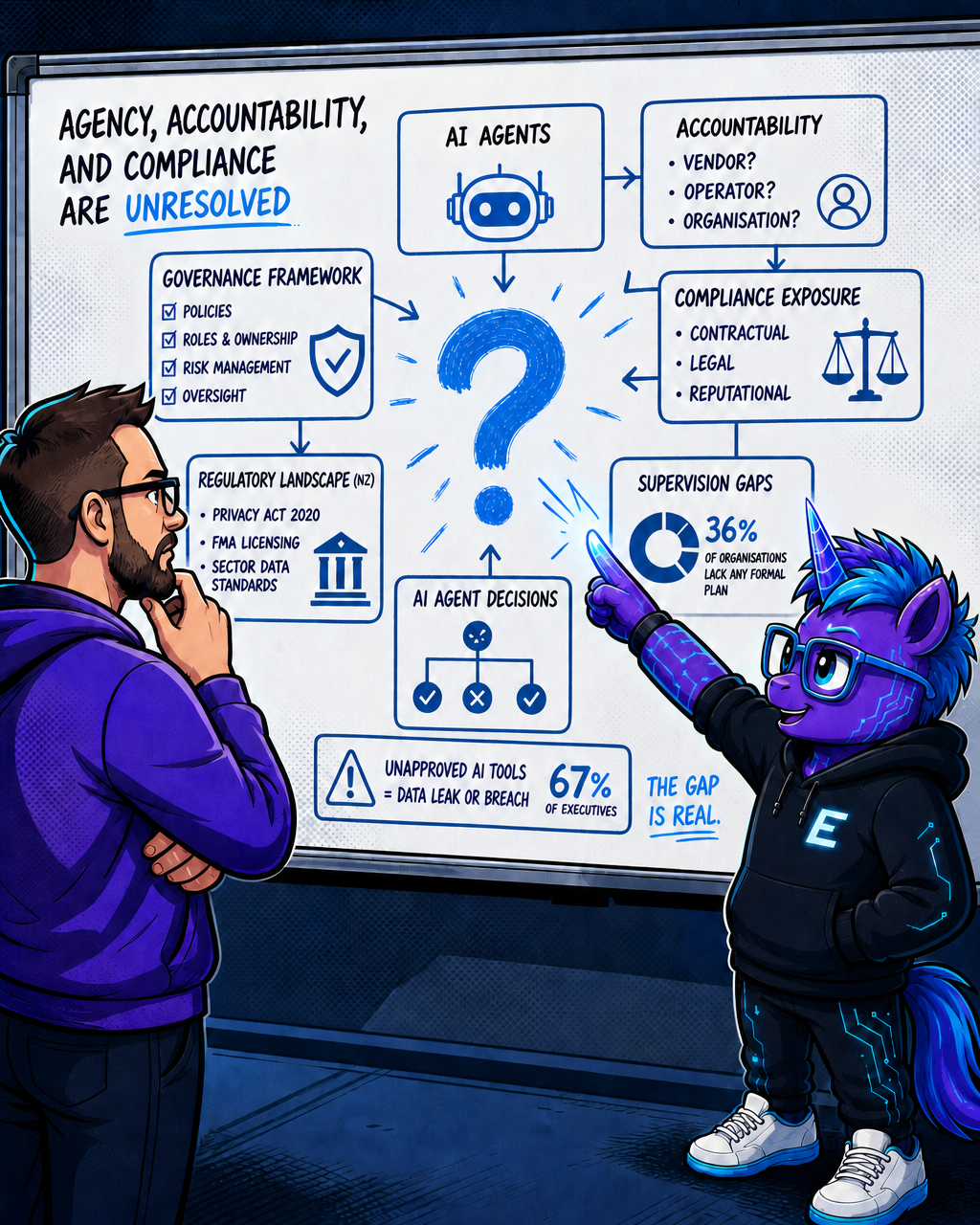

Agency, Accountability, and Compliance Are Unresolved

There's a quieter set of risks that don't show up in funding charts but will show up in board risk registers.

As AI agents move from experiment to deployment, governance is emerging as a serious unresolved problem. In 2026, 67% of executives believe their company has already suffered a data leak or breach due to unapproved AI tools. Meanwhile, 36% of organisations lack any formal plan for supervising AI agents at all.

In regulated industries — financial services, healthcare, government — the compliance exposure from AI agent behaviour is not theoretical. It's contractual, legal, and reputational. AI agents make decisions. When those decisions are wrong, who is accountable? The vendor? The operator? The organisation that deployed it?

These questions don't have clear answers yet. In the NZ context, obligations under the Privacy Act 2020, FMA licensing requirements, and sector-specific data standards all create exposure that a general-purpose AI deployment doesn't address by default. The same gap exists across ANZ regulated verticals.

This isn't an argument against AI adoption. It's an argument that the current valuation environment is not pricing in the compliance friction that enterprise adoption at scale will generate. That friction is real and it slows the return timelines the optimists are counting on.

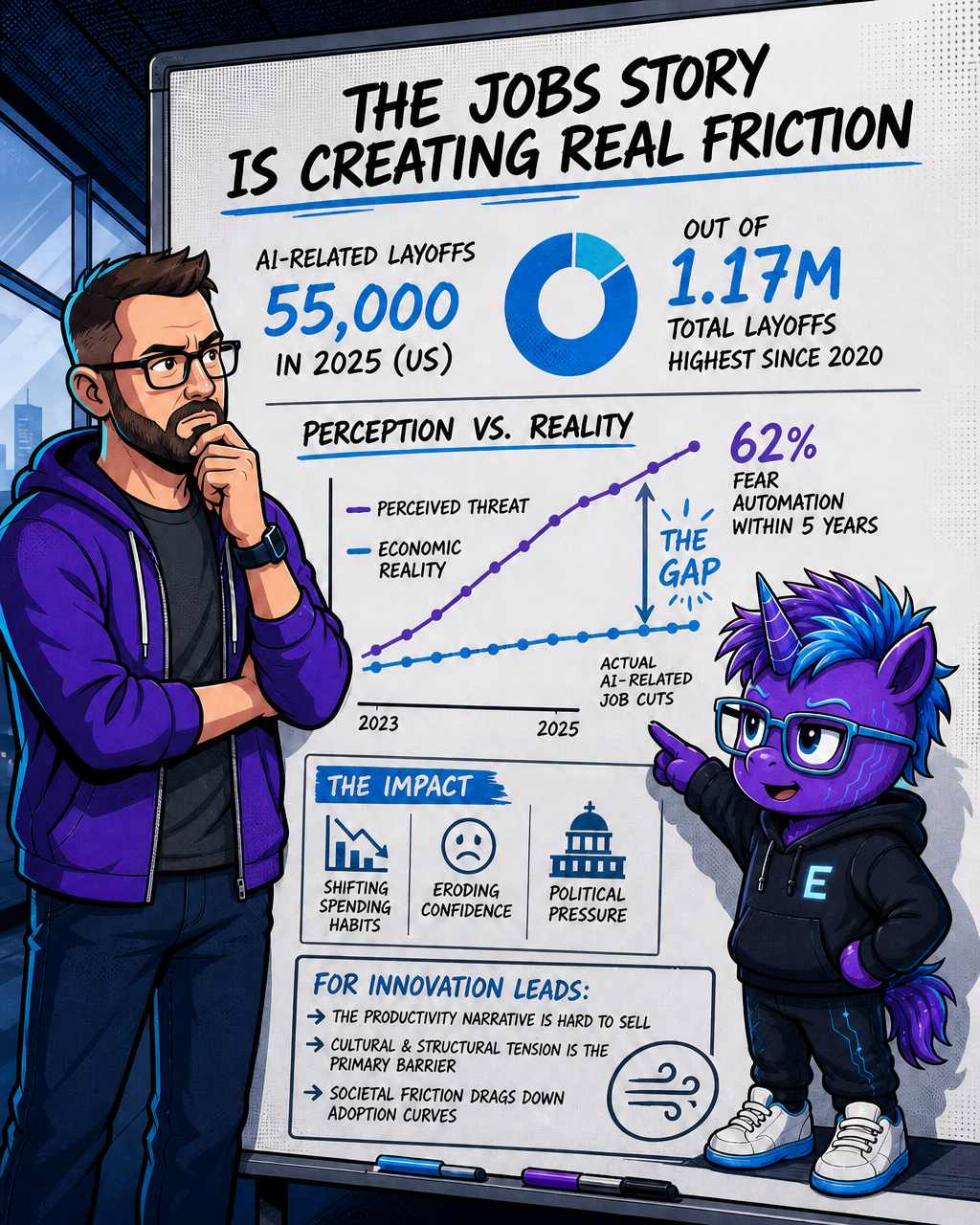

The Jobs Story Is Creating Real Friction

AI job displacement is happening, but not at the apocalyptic pace that generates the most online traffic.

In 2025, approximately 55,000 job cuts in the US were directly attributed to AI, according to Challenger, Gray and Christmas, out of a total 1.17 million layoffs — the highest since 2020. The labour substitution effects are described by most economists as creeping in slowly and unevenly across occupations, rather than dramatically.

But public perception doesn't track the economics. A 2025 Pew Research survey found 62% of white-collar workers fear job automation within five years, up from 45% in 2023. That fear is shifting spending habits, eroding confidence, and creating genuine political pressure on AI deployment in enterprise settings.

For innovation leads trying to champion AI internally, this is a real headwind. The productivity narrative is hard to sell to teams who interpret "efficiency gains" as code for headcount reduction. The cultural and structural tension inside organisations is now a primary barrier to enterprise deployment — not the technology.

That societal friction creates a drag on the adoption curves that the market's current valuations assume.

A Correction Is Not a Collapse

Here's where reasonable people can take a clear-eyed position without either cheerleading or catastrophising.

The technology is genuinely transformative. The internet was too. The technology surviving a market correction is exactly what happened with the dot-com bust — and the companies that were real, with real revenue and real infrastructure, are still standing 25 years later.

What a correction resets is not AI's long-term relevance. It resets expectations, clears the speculative froth from early-stage valuations, and concentrates capital in the companies that can actually demonstrate returns. Some bubbles will burst, but the core thesis may still hold.

The organisations that are building with AI right now — carefully, with proper governance, with implementation discipline — are not necessarily in the bubble. The bubble is in the valuation of companies that can't yet demonstrate they'll still be relevant when enterprise adoption actually reaches scale.

For anyone allocating capital or making AI deployment decisions in 2026: the question isn't whether to engage with AI. The question is whether you're pricing in realistic timelines, building proper governance from the start, and measuring outcomes that actually show up in the numbers — not just in the pilot.

That's a pretty good question to have going into the second half of the year.

What This Means If You're Building Right Now

At Evotron Studio, we build AI-enabled products for domain-expert founders. That means we've had to work through the governance questions, the compliance questions, and the "what happens when the agent gets it wrong" questions — on our own products, before engaging with clients.

If you're a domain-expert founder in NZ or ANZ and you're watching the AI market with a mix of interest and scepticism, that's a reasonable posture. The technology is real. The hype around it is not a reliable guide to what actually works in a regulated NZ market.

Want to talk about what a pragmatic, accountable AI-enabled build looks like for your venture? Start the conversation at Evotron Studio.

Evotron Studio

We build and run our own AI-amplified ventures — and bring the same capability into yours.

We build and run our own AI-amplified ventures — and bring the same capability into yours.

Learn more about Evotron Studio and get started today.

Visit Evotron Studio